from mywebstyle import plot_styleimport matplotlib.pyplot as pltimport seaborn as snsimport numpy as npimport pandas as pdimport kaggle'#f4f4f4' )= pd.read_csv('lending_club_loan_two.csv' )= loandata.iloc[:, :13 ]

Warning: Your Kaggle API key is readable by other users on this system! To fix this, you can run 'chmod 600 /Users/macpc/.kaggle/kaggle.json'

0

10000

36 months

11.44

329.48

B

B4

Marketing

10+ years

RENT

117000.0

Not Verified

Jan-15

Fully Paid

1

8000

36 months

11.99

265.68

B

B5

Credit analyst

4 years

MORTGAGE

65000.0

Not Verified

Jan-15

Fully Paid

2

15600

36 months

10.49

506.97

B

B3

Statistician

< 1 year

RENT

43057.0

Source Verified

Jan-15

Fully Paid

3

7200

36 months

6.49

220.65

A

A2

Client Advocate

6 years

RENT

54000.0

Not Verified

Nov-14

Fully Paid

4

24375

60 months

17.27

609.33

C

C5

Destiny Management Inc.

9 years

MORTGAGE

55000.0

Verified

Apr-13

Charged Off

= loandata.iloc[:, 13 :]

0

vacation

Vacation

26.24

Jun-90

16

0

36369

41.8

25

w

INDIVIDUAL

0.0

0.0

0174 Michelle Gateway\r\nMendozaberg, OK 22690

1

debt_consolidation

Debt consolidation

22.05

Jul-04

17

0

20131

53.3

27

f

INDIVIDUAL

3.0

0.0

1076 Carney Fort Apt. 347\r\nLoganmouth, SD 05113

2

credit_card

Credit card refinancing

12.79

Aug-07

13

0

11987

92.2

26

f

INDIVIDUAL

0.0

0.0

87025 Mark Dale Apt. 269\r\nNew Sabrina, WV 05113

3

credit_card

Credit card refinancing

2.60

Sep-06

6

0

5472

21.5

13

f

INDIVIDUAL

0.0

0.0

823 Reid Ford\r\nDelacruzside, MA 00813

4

credit_card

Credit Card Refinance

33.95

Mar-99

13

0

24584

69.8

43

f

INDIVIDUAL

1.0

0.0

679 Luna Roads\r\nGreggshire, VA 11650

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 395900 entries, 0 to 395899

Data columns (total 27 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 loan_amnt 395900 non-null int64

1 term 395900 non-null object

2 int_rate 395900 non-null float64

3 installment 395900 non-null float64

4 grade 395900 non-null object

5 sub_grade 395900 non-null object

6 emp_title 372982 non-null object

7 emp_length 377608 non-null object

8 home_ownership 395900 non-null object

9 annual_inc 395900 non-null float64

10 verification_status 395900 non-null object

11 issue_d 395900 non-null object

12 loan_status 395900 non-null object

13 purpose 395900 non-null object

14 title 394145 non-null object

15 dti 395900 non-null float64

16 earliest_cr_line 395900 non-null object

17 open_acc 395900 non-null int64

18 pub_rec 395900 non-null int64

19 revol_bal 395900 non-null int64

20 revol_util 395624 non-null float64

21 total_acc 395900 non-null int64

22 initial_list_status 395900 non-null object

23 application_type 395900 non-null object

24 mort_acc 358117 non-null float64

25 pub_rec_bankruptcies 395365 non-null float64

26 address 395900 non-null object

dtypes: float64(7), int64(5), object(15)

memory usage: 81.6+ MB

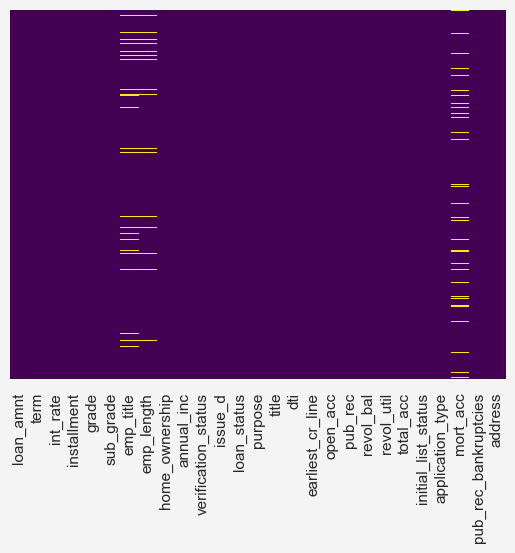

= False , cbar= False , cmap= 'viridis' )

loan_amnt

395900.0

14114.249305

8357.637338

500.00

8000.00

12000.00

20000.00

40000.00

int_rate

395900.0

13.639385

4.472112

5.32

10.49

13.33

16.49

30.99

installment

395900.0

431.859947

250.733444

16.08

250.33

375.43

567.30

1533.81

annual_inc

395900.0

74206.819251

61645.032777

0.00

45000.00

64000.00

90000.00

8706582.00

dti

395900.0

17.379187

18.021550

0.00

11.28

16.91

22.98

9999.00

open_acc

395900.0

11.311081

5.137591

0.00

8.00

10.00

14.00

90.00

pub_rec

395900.0

0.178204

0.530716

0.00

0.00

0.00

0.00

86.00

revol_bal

395900.0

15844.331435

20589.846553

0.00

6026.00

11181.00

19620.00

1743266.00

revol_util

395624.0

53.793449

24.452575

0.00

35.80

54.80

72.90

892.30

total_acc

395900.0

25.414622

11.887279

2.00

17.00

24.00

32.00

151.00

mort_acc

358117.0

1.814091

2.148006

0.00

0.00

1.00

3.00

34.00

pub_rec_bankruptcies

395365.0

0.121647

0.356176

0.00

0.00

0.00

0.00

8.00

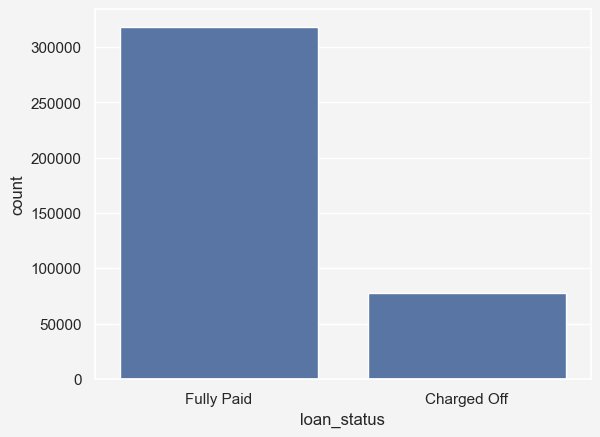

= 'loan_status' , data= loandata)= np.round (len (loandata[loandata['loan_status' ] == 'Fully Paid' ])/ len (loandata)* 100 , 2 = np.round (len (loandata[loandata['loan_status' ] == 'Charged Off' ]) / len (loandata)* 100 , 2

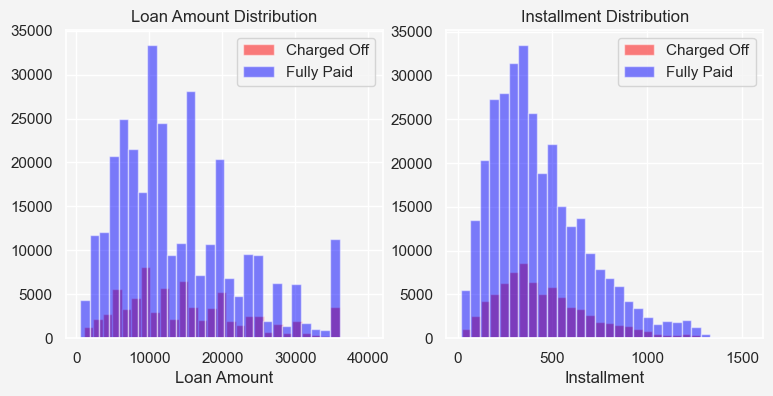

= plt.figure(figsize= (9 , 4 ))= fig.add_subplot(121 )'loan_status' ] == 'Charged Off' ]['loan_amnt' ].hist(= 0.5 , color= 'red' , bins= 30 , ax= ax1,= 'Charged Off' 'loan_status' ] == 'Fully Paid' ]['loan_amnt' ].hist(= 0.5 , color= 'blue' , bins= 30 , ax= ax1,= 'Fully Paid' 'Loan Amount Distribution' )'Loan Amount' )= fig.add_subplot(122 )'loan_status' ] == 'Charged Off' ]['installment' ].hist(= 0.5 , color= 'red' , bins= 30 , ax= ax2,= 'Charged Off' 'loan_status' ] == 'Fully Paid' ]['installment' ].hist(= 0.5 , color= 'blue' , bins= 30 , ax= ax2,= 'Fully Paid' 'Installment Distribution' )'Installment' )

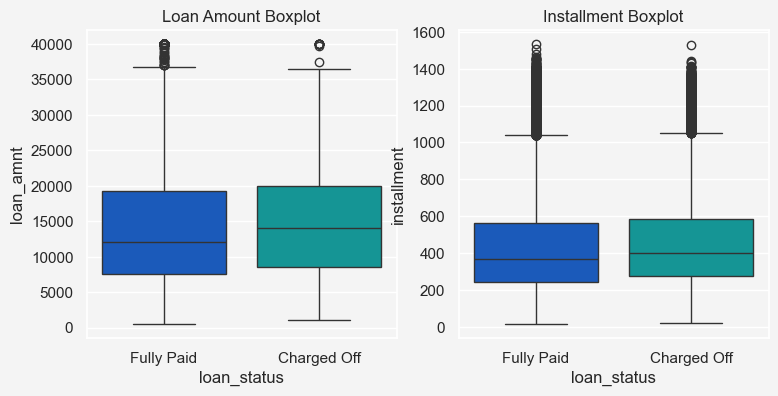

= plt.figure(figsize= (8.8 , 4 ))= fig.add_subplot(121 )= 'loan_status' , y= 'loan_amnt' , hue= 'loan_status' ,= loandata, ax= ax1, palette= 'winter' 'Loan Amount Boxplot' )= fig.add_subplot(122 )= 'loan_status' , y= 'installment' , hue= 'loan_status' ,= loandata, ax= ax2, palette= 'winter' 'Installment Boxplot' )

Text(0.5, 1.0, 'Installment Boxplot')

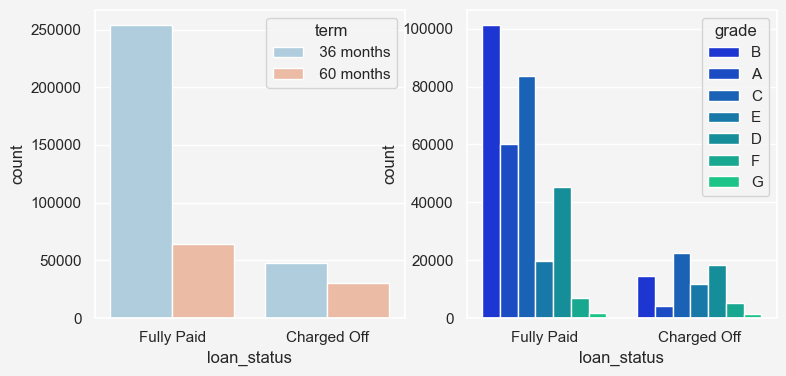

= plt.figure(figsize= (8.8 , 4 ))= fig.add_subplot(121 )= 'loan_status' ,= 'term' , data= loandata,= 'RdBu_r' , ax= ax1= fig.add_subplot(122 )= 'loan_status' ,= 'grade' , data= loandata,= 'winter' , ax= ax2

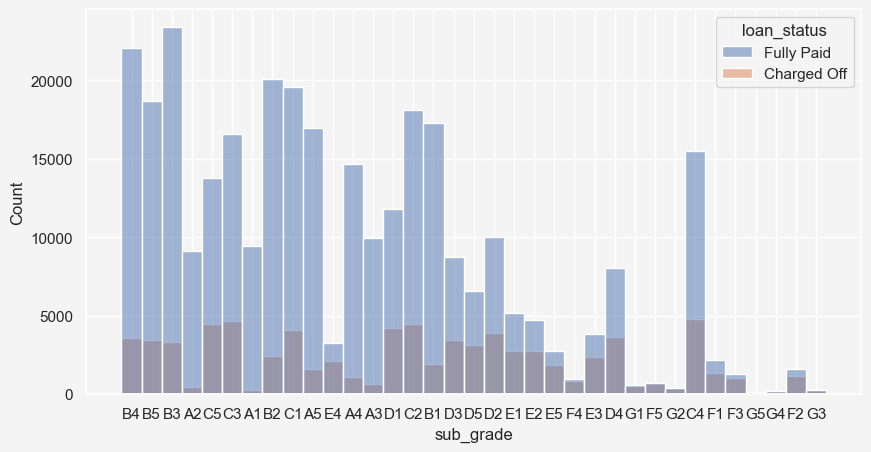

= plt.subplots(figsize= (10 , 5 ))= 'sub_grade' , hue= 'loan_status' , data= loandata, ax= ax)

'emp_title' ] = loandata['emp_title' ].str .lower()25 ]

emp_title

manager 5635

teacher 5426

registered nurse 2626

supervisor 2589

sales 2381

driver 2306

owner 2200

rn 2072

project manager 1776

office manager 1638

general manager 1460

truck driver 1288

director 1192

engineer 1187

police officer 1041

vice president 961

sales manager 961

operations manager 960

store manager 941

president 877

administrative assistant 865

accountant 845

account manager 845

technician 839

mechanic 753

Name: count, dtype: int64

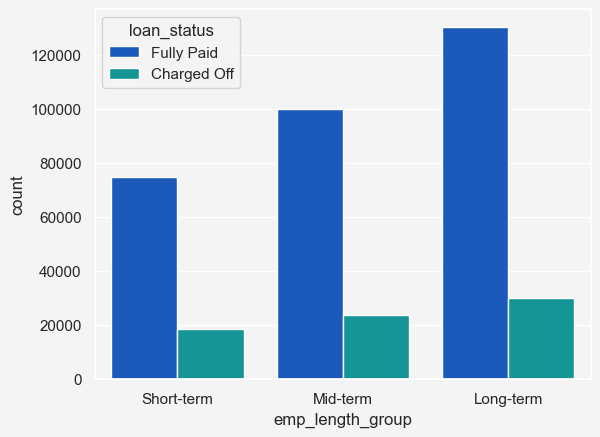

'future.no_silent_downcasting' , True )'emp_length' ] = loandata['emp_length' ].replace({'< 1 year' : 0 ,'1 year' : 1 ,'2 years' : 2 ,'3 years' : 3 ,'4 years' : 4 ,'5 years' : 5 ,'6 years' : 6 ,'7 years' : 7 ,'8 years' : 8 ,'9 years' : 9 ,'10+ years' : 10 = False )'emp_length_group' ] = pd.cut('emp_length' ],= [- 1 , 2 , 7 , 10 ], # Bins: <3 years, 3-7 years, > 7 years = ['Short-term' , 'Mid-term' , 'Long-term' ]= 'emp_length_group' ,= 'loan_status' ,= loandata,= 'winter' ,= 'count'

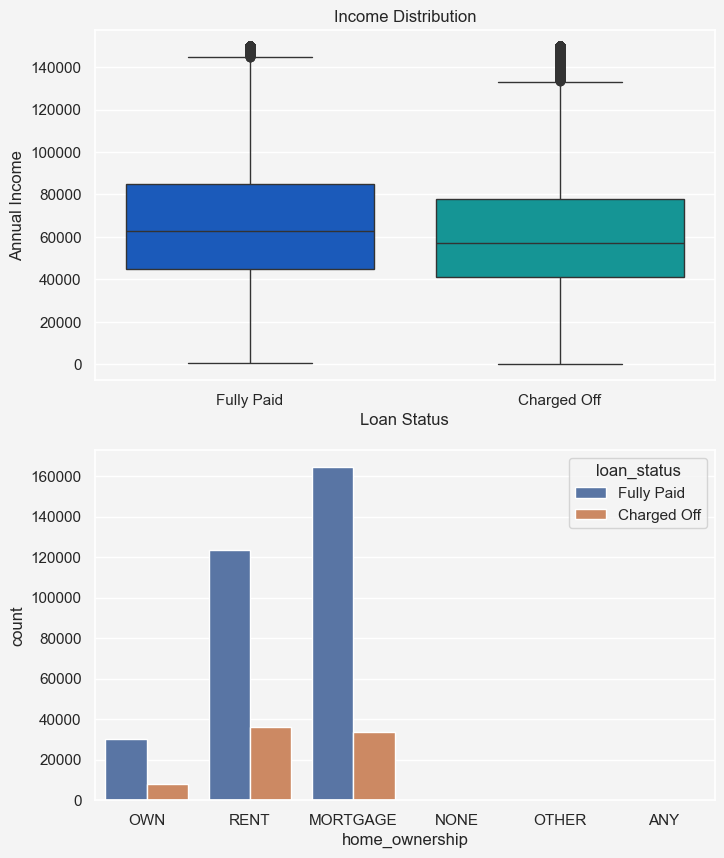

= plt.figure(figsize= (8 , 10 ))= fig.add_subplot(211 )= loandata['annual_inc' ].quantile(0.95 )= loandata[loandata['annual_inc' ] <= annual_income_threshod]= 'loan_status' , y= 'annual_inc' ,= 'loan_status' , palette= 'winter' ,= filtered_income, ax= ax1'Income Distribution' )'Loan Status' )'Annual Income' )= fig.add_subplot(212 )= 'home_ownership' , hue= 'loan_status' ,= loandata, ax= ax2

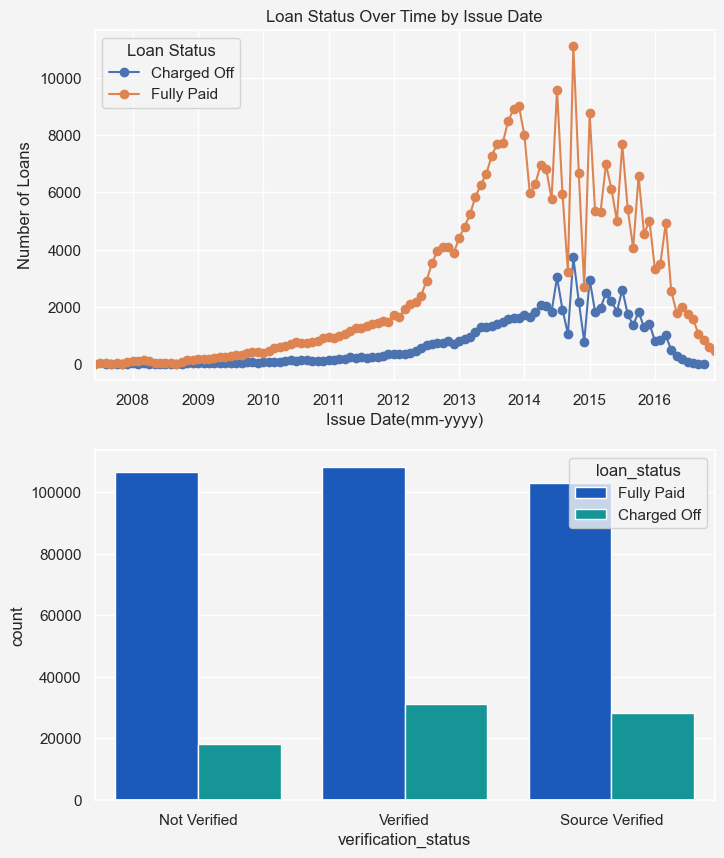

'issue_d' ] = pd.to_datetime('issue_d' ], format = '%b-%y' = loandata.sort_values('issue_d' )= loandata.groupby('issue_d' , 'loan_status' ]).size().unstack()= plt.figure(figsize= (8 , 10 ))= fig.add_subplot(211 )= 'line' , marker= 'o' , ax= ax1'Loan Status Over Time by Issue Date' )'Issue Date(mm-yyyy)' )'Number of Loans' )= 'Loan Status' )= fig.add_subplot(212 )= 'verification_status' , hue= 'loan_status' ,= loandata, palette= 'winter' , ax= ax2

'purpose' ].value_counts()

purpose

debt_consolidation 234420

credit_card 82998

home_improvement 24024

other 21177

major_purchase 8788

small_business 5701

car 4696

medical 4194

moving 2853

vacation 2452

house 2201

wedding 1811

renewable_energy 328

educational 257

Name: count, dtype: int64

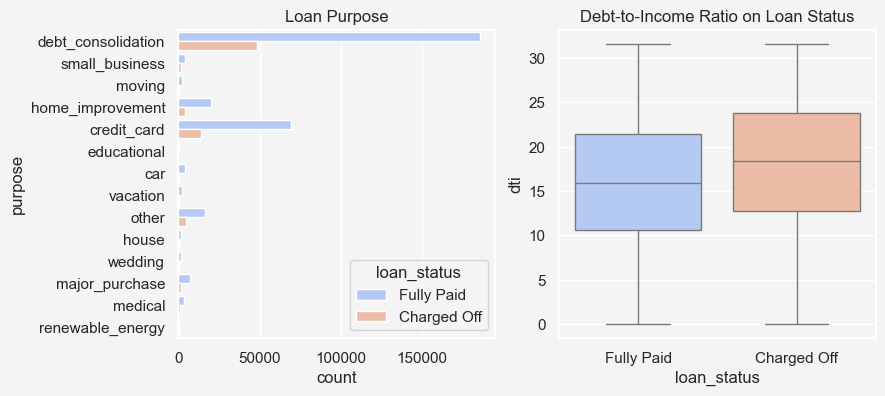

= plt.figure(figsize= (9 , 4 ))= fig.add_subplot(121 )= 'purpose' , hue= 'loan_status' ,= loandata, palette= 'coolwarm' 'Loan Purpose' )= fig.add_subplot(122 )= loandata['dti' ].quantile(0.95 )= loandata[loandata['dti' ] <= dti_threshold]= 'loan_status' , y= 'dti' ,= 'loan_status' , data= filtereddata,= 'coolwarm' , ax= ax2'Debt-to-Income Ratio on Loan Status' )

Text(0.5, 1.0, 'Debt-to-Income Ratio on Loan Status')

Insights: From the purpose column, we see that most of the loans that were charged off were used to make debt consolidation. Therefore, debt consolidation may have been a significant factor when a loan is charged off. Another insight we obtain from the debt-to-income ratio is that the charged off loans have higher dti ratio

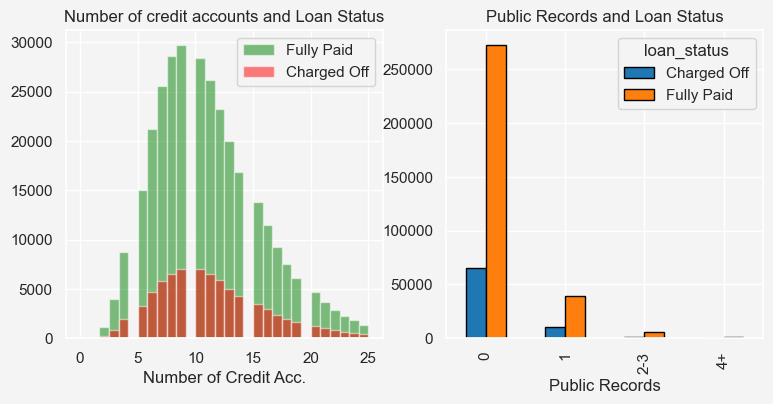

= plt.figure(figsize= (9 , 4 ))= fig.add_subplot(121 )= loandata['open_acc' ].quantile(0.98 )= loandata[loandata['open_acc' ]<= filtered_open_account_threshold]'loan_status' ] == 'Fully Paid' ]['open_acc' ].hist(= 0.5 , color= 'green' , bins= 30 , label= 'Fully Paid' , ax= ax1'loan_status' ] == 'Charged Off' ]['open_acc' ].hist(= 0.5 , color= 'red' , bins= 30 , label= 'Charged Off' , ax= ax1'Number of Credit Acc.' )'Number of credit accounts and Loan Status' )'pub_rec_group' ] = pd.cut('pub_rec' ], bins= [- 1 , 0 , 1 , 3 , loandata['pub_rec' ].max ()],= ['0' , '1' , '2-3' , '4+' ]= loandata.groupby('pub_rec_group' , 'loan_status' ], observed= False = fig.add_subplot(122 )= 'bar' , stacked= False , edgecolor= 'black' ,= ['#1f77b4' , '#ff7f0e' ], ax= ax2'Public Records and Loan Status' )'Public Records' )

Text(0.5, 0, 'Public Records')

= 'open_acc' , x= 'loan_status' ,= 'loan_status' ,= filtered_open_account

Insights: Number of credit account seems normally distributed among both groups except for some outliers. However, the mean number of credit accounts are slightly higher for the charged off category than the fully paid category. So, higher credit account has some sort of relation with loan being charged off. Also, people who doesn’t have any public record seems to have higher chance of loan status being charged off

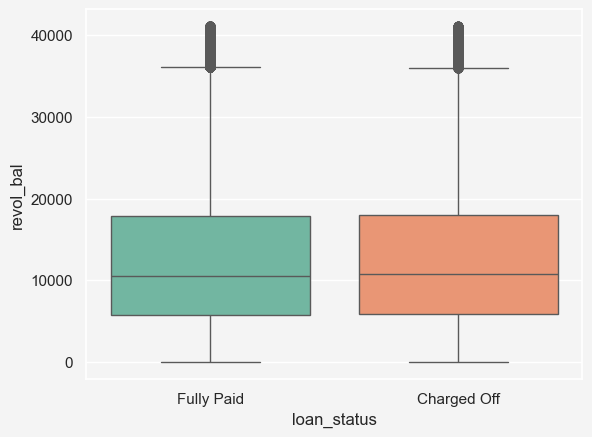

= loandata['revol_bal' ].quantile(0.95 )= loandata[loandata['revol_bal' ] <= revol_bal_threshold]= 'loan_status' , y= 'revol_bal' ,= filtered_revol_bal, hue= 'loan_status' ,= 'Set2'

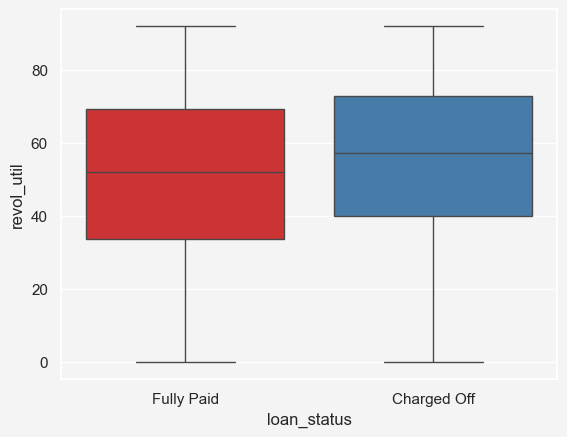

= loandata['revol_util' ].quantile(0.95 )= loandata[loandata['revol_util' ] <= revol_util_threshold]= 'loan_status' , y= 'revol_util' ,= 'loan_status' , data= filtered_revol_util,= 'Set1'

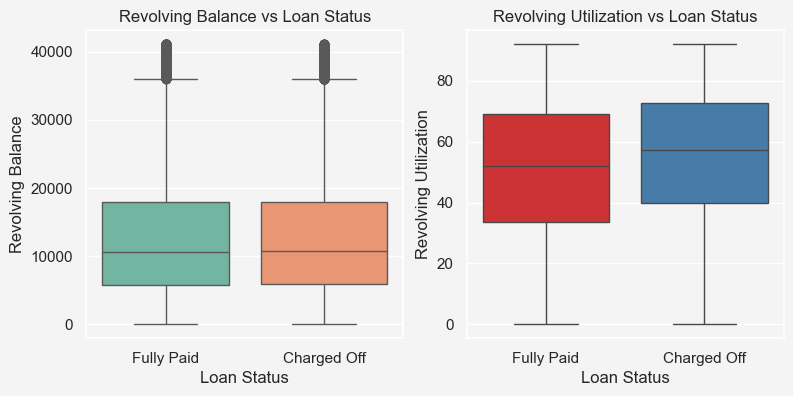

= plt.figure(figsize= (9 , 4 ))= fig.add_subplot(121 )= loandata['revol_bal' ].quantile(0.95 )= loandata[loandata['revol_bal' ] <= revol_bal_threshold]= 'loan_status' , y= 'revol_bal' ,= filtered_revol_bal, hue= 'loan_status' ,= 'Set2' , ax= ax1'Loan Status' )'Revolving Balance' )'Revolving Balance vs Loan Status' )= fig.add_subplot(122 )= loandata['revol_util' ].quantile(0.95 )= loandata[loandata['revol_util' ] <= revol_util_threshold]= 'loan_status' , y= 'revol_util' ,= 'loan_status' , data= filtered_revol_util,= 'Set1' , ax= ax2'Loan Status' )'Revolving Utilization' )'Revolving Utilization vs Loan Status' )

Text(0.5, 1.0, 'Revolving Utilization vs Loan Status')

'total_acc' ].value_counts()

total_acc

21 14274

22 14255

20 14220

23 13915

24 13874

...

151 1

104 1

135 1

108 1

115 1

Name: count, Length: 118, dtype: int64

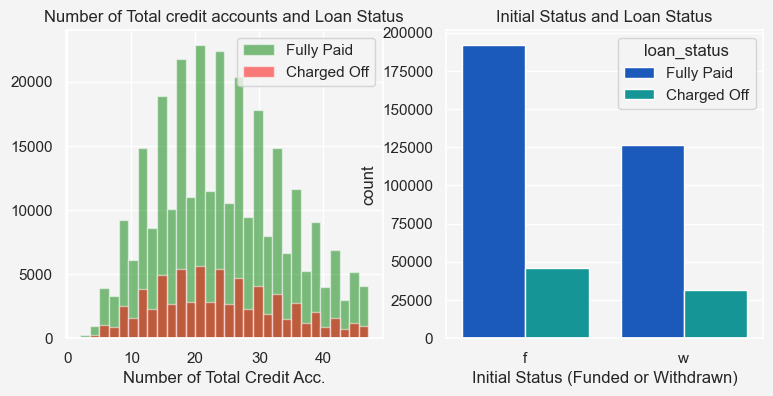

= plt.figure(figsize= (9 , 4 ))= fig.add_subplot(121 )= loandata['total_acc' ].quantile(0.95 )= loandata[loandata['total_acc' ]<= filtered_total_account_threshold]'loan_status' ] == 'Fully Paid' ]['total_acc' ].hist(= 0.5 , color= 'green' , bins= 30 , label= 'Fully Paid' , ax= ax1'loan_status' ] == 'Charged Off' ]['total_acc' ].hist(= 0.5 , color= 'red' , bins= 30 , label= 'Charged Off' , ax= ax1'Number of Total Credit Acc.' )'Number of Total credit accounts and Loan Status' )= fig.add_subplot(122 )= 'initial_list_status' , hue= 'loan_status' ,= loandata, palette= 'winter' 'Initial Status and Loan Status' )'Initial Status (Funded or Withdrawn)' )

Text(0.5, 0, 'Initial Status (Funded or Withdrawn)')

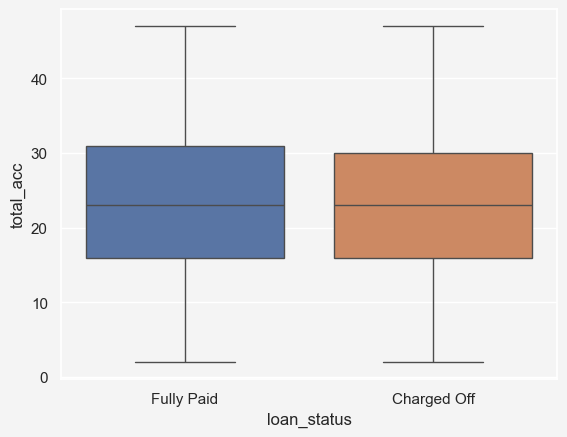

= 'total_acc' , x= 'loan_status' ,= 'loan_status' ,= filtered_total_account

'application_type' ].value_counts()

application_type

INDIVIDUAL 395189

JOINT 425

DIRECT_PAY 286

Name: count, dtype: int64

'mort_acc' ].value_counts()

mort_acc

0.0 139727

1.0 60392

2.0 49931

3.0 38040

4.0 27880

5.0 18188

6.0 11067

7.0 6050

8.0 3121

9.0 1655

10.0 865

11.0 479

12.0 264

13.0 146

14.0 107

15.0 61

16.0 37

17.0 22

18.0 18

19.0 15

20.0 13

24.0 10

22.0 7

25.0 4

21.0 4

27.0 3

23.0 2

31.0 2

32.0 2

26.0 2

34.0 1

30.0 1

28.0 1

Name: count, dtype: int64

= loandata.groupby('loan_status' )['mort_acc' ].describe()print (mort_acc_summary)

count mean std min 25% 50% 75% max

loan_status

Charged Off 72103.0 1.501214 1.974335 0.0 0.0 1.0 2.0 23.0

Fully Paid 286014.0 1.892967 2.182550 0.0 0.0 1.0 3.0 34.0

# Bin the mort_acc column into categories 'mort_acc_group' ] = pd.cut('mort_acc' ], bins= [- 1 , 0 , 2 , 5 , 10 , loandata['mort_acc' ].max ()],= ['0' , '1-2' , '3-5' , '6-10' , '10+' ]# Plot the grouped bar chart = loandata.groupby('mort_acc_group' , 'loan_status' ], observed= False = 'bar' , stacked= False ,= (10 , 6 ), colormap= 'viridis' )'Loan Status by Number of Mortgage Accounts' )'Number of Mortgage Accounts (Grouped)' )'Number of Loans' )= 0 )= 'Loan Status' )

'pub_rec_bankruptcies' ].value_counts()

pub_rec_bankruptcies

0.0 350265

1.0 42776

2.0 1846

3.0 351

4.0 82

5.0 32

6.0 7

7.0 4

8.0 2

Name: count, dtype: int64

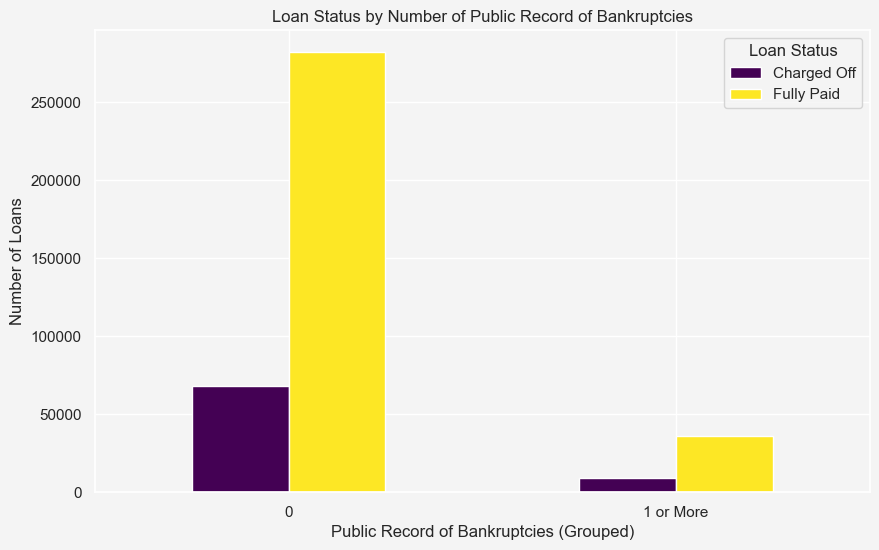

'pub_rec_bankruptcies_group' ] = pd.cut('pub_rec_bankruptcies' ], bins= [- 1 , 0 ,'pub_rec_bankruptcies' ].max ()],= ['0' , '1 or More' ]# Plot the grouped bar chart = loandata.groupby('pub_rec_bankruptcies_group' , 'loan_status' ], observed= False = 'bar' , stacked= False , figsize= (10 , 6 ), colormap= 'viridis' )'Loan Status by Number of Public Record of Bankruptcies' )'Public Record of Bankruptcies (Grouped)' )'Number of Loans' )= 0 )= 'Loan Status' )

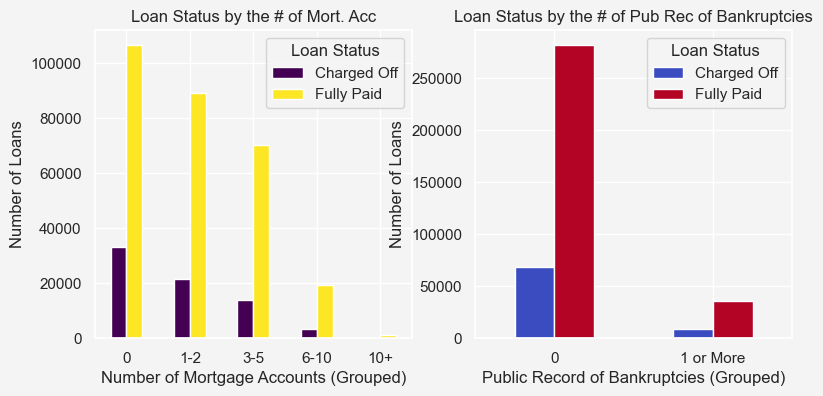

= plt.figure(figsize= (9 , 4 ))= fig.add_subplot(121 )'mort_acc_group' ] = pd.cut('mort_acc' ], bins= [- 1 , 0 , 2 , 5 , 10 , loandata['mort_acc' ].max ()],= ['0' , '1-2' , '3-5' , '6-10' , '10+' ]= loandata.groupby('mort_acc_group' , 'loan_status' ], observed= False = 'bar' , stacked= False ,= 'viridis' , ax= ax1'Loan Status by the # of Mort. Acc' )'Number of Mortgage Accounts (Grouped)' )'Number of Loans' )= 0 )= 'Loan Status' )= fig.add_subplot(122 )'pub_rec_bankruptcies_group' ] = pd.cut('pub_rec_bankruptcies' ], bins= [- 1 , 0 ,'pub_rec_bankruptcies' ].max ()],= ['0' , '1 or More' ]# Plot the grouped bar chart = loandata.groupby('pub_rec_bankruptcies_group' , 'loan_status' ], observed= False = 'bar' , stacked= False ,= 'coolwarm' , ax= ax2'Loan Status by the # of Pub Rec of Bankruptcies' )'Public Record of Bankruptcies (Grouped)' )'Number of Loans' )= 0 )= 'Loan Status' )

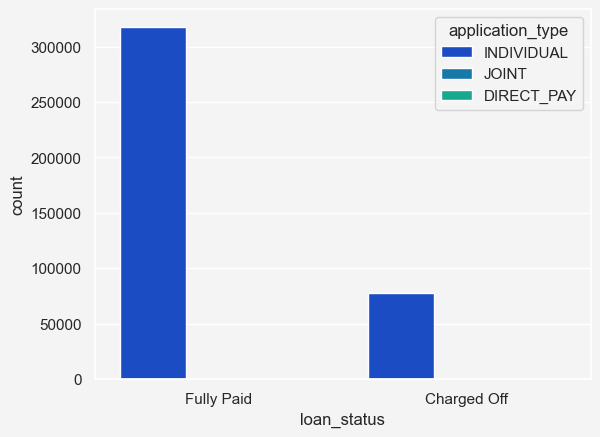

'application_type' ].value_counts()

application_type

INDIVIDUAL 395189

JOINT 425

DIRECT_PAY 286

Name: count, dtype: int64

= 'loan_status' , hue= 'application_type' , = loandata, palette= 'winter'

= loandata.select_dtypes(include= ['float64' ,'int64' ])= (10 ,8 ))= True , cmap= 'coolwarm' , vmin=- 1 , vmax= 1 )